How do I extend my form 5227?

Also to know is, can you file Form 5227 electronically?

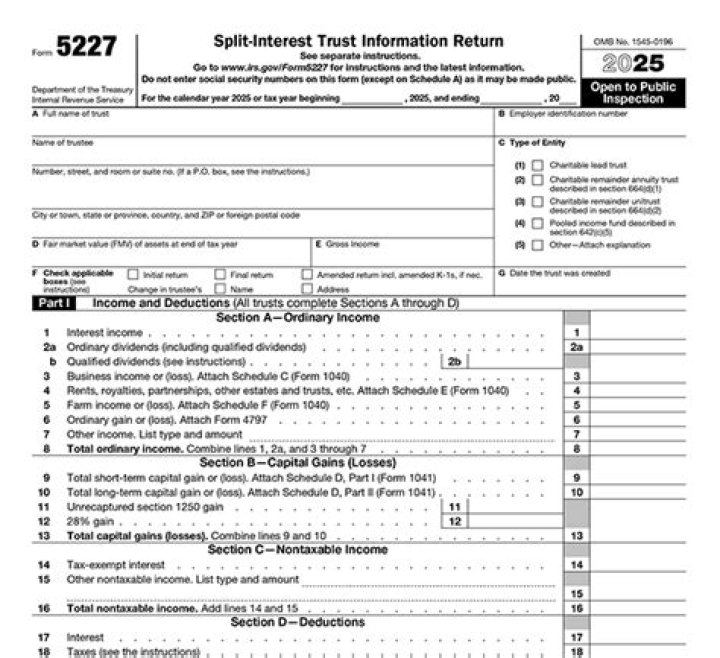

Form 5227, Split-Interest Trust Information Return, cannot be e-filed. The form is available in the 1041 fiduciary return by completing applicable screens on the 5227 tab. The presence of a Form 5227 does not prevent e-filing a 1041, but the 5227 is not transmitted with the 1041.

Similarly, what is the 5227 form used for? Use Form 5227 to: Report the financial activities of a split-interest trust. Provide certain information regarding charitable deductions and distributions of or from a split-interest trust. Determine if the trust is treated as a private foundation and subject to certain excise taxes under Chapter 42.

Beside above, what form do I use to file an extension for a trust?

Use Form 8736 to request an automatic 3-month extension of time to file a return for: Trusts filing Form 1041, U.S. Income Tax Return for Estates and Trusts, Form 1041-N, U.S. Income Tax Return for Electing Alaska Native Settlement Trusts, or Form 1041-QFT, U.S. Income Tax Return for Qualified Funeral Trusts.

Does a charitable remainder trust file a Form 1041?

A split-interest trust other than an IRC Section 664 charitable remainder trust must file Form 1041 with Form 5227 if it has $600 of gross income or any taxable income during the year. For charitable remainder trusts, there is no requirement that the named charity even know of its impending gift.

Related Question Answers

What is the extended due date for Form 5227?

File Form 5227 for calendar year 2020 by April 15, 2021. In the case of a final short-year period, the return is due by the 15th day of the 4th month following the date of the trust's termination. Extension of time to file. Use Form 8868 to request an automatic extension of time to file.Can I file Form 7004 online?

Form 7004 can be e-filed through the Modernized e-File (MeF) platform. All the returns shown on Form 7004 are eligible for an automatic extension of time to file from the due date of the return. The Form 7004 does not extend the time for payment of tax.Where do I send my 7004 extension?

THEN file Form 7004 at: Internal Revenue Service, P.O. Box 409101, Ogden, UT 84409. AND your principal business, office, or agency is located inHow do I file an extension for my non profit taxes?

Tax-exempt organizations can use IRS Form 8868 (Application for Extension of Time to File an Exempt Organization Return) to request an automatic 3-month tax extension. Form 8868 can also be used to apply for an additional 3-month (non-automatic) tax extension if the first 3 months weren't enough.Are Form 990s extended?

The due date for filing Form 990 series returns and most other returns that were due between April 1, 2020 and July 15, 2020 has been extended to July 15, 2020. In addition, the deadline for payment of tax reported on Forms 990-T, 990-PF, 990-W, and Form 4720 is extended to July 15.How long does form 7004 extend?

6-monthAre partnership tax returns extended?

For individuals, that means you can still file for a tax extension right on April 15. The same goes for businesses: S corps and partnerships can still get an extension on March 15, and the last day for C corps to file for an extension is April 15. Read on for a detailed list of every tax deadline in 2021.Can you file Form 7004 late?

Avoid IRS Late Filing PenaltiesIf you fail to file either IRS Form 7004 or business tax return by the appropriate filing deadline (March 15th for S Corps, Multi Member LLC's and Partnerships and April 15th for C Corporations), the IRS will charge interest and penalties on any unpaid Federal taxes.

How many times can you extend a 990?

An organization will only be allowed an extension of 6 months for a return for a tax year. Note that Form 8868 cannot be filed to extend the due date of a Form 990-N. Extending the time for filing a return does not extend the time for paying tax.How do I file an IRS extension?

How to request an extension to file- File Form 4868 through their tax professional, tax software or using Free File on IRS.gov.

- Submit an electronic payment with Direct Pay, Electronic Federal Tax Payment System or by debit, credit card or digital wallet and select Form 4868 or extension as the payment type.

Is a charitable remainder trust tax exempt?

A charitable remainder trust is a tax-exempt irrevocable trust designed to reduce the taxable income of individuals. A charitable remainder trust allows a trustor to make contributions, be eligible for a tax deduction, and donate a portion of the assets.Are CRUTs tax exempt?

Often, CRUTs can be used to save income, gift, and/or estate tax. Because the CRUT is a tax-exempt entity a CRUT can be used to sell highly appreciated assets at greatly reduced tax consequences.How long can a charitable remainder trust last?

A CRT may last for the Lead Beneficiaries' joint lives or for a term of years (the term may not exceed 20 years). In addition, the actuarial value of the CRT remainder left to charity must be least 10% of the initial CRT value, determined at time of funding.Is a charitable remainder trust included in gross estate?

If an individual establishes a charitable remainder trust for his or her life only, the trust assets will be included in his or her gross estate under IRC section 2036. The amount included, however, will “wash out” as an estate tax charitable deduction under IRC section 2055.Do Charitable Trusts file tax returns?

The income tax return of Charitable Trusts must be filed using ITR 5 or ITR 7. In case the Trust is required to file an income tax return due to taxable income being in excess of the basic exemption limit, then ITR 5 can be filed.How do you terminate a charitable remainder trust?

Three Ways to Terminate a CRT Early- Donating all or an undivided fractional portion of the income interest to the charitable remainder beneficiary.

- “Cashing in” all or a portion of the income interest.

- Selling to an unrelated third party.